Private real estate notes are debt instruments secured by real property that let investors earn income by collecting payments without owning the physical property. Known formally as mortgage notes or promissory notes, they represent a borrower's written promise to repay a loan, with real estate pledged as collateral. Performing notes yield 7%–14% annually, while non-performing notes target returns of 15%–50% or more. That yield gap reflects the difference in risk, not just reward. Investors who understand lien position, collateral value, and borrower status can build a cash-flowing portfolio without ever dealing with tenants, toilets, or maintenance calls.

What do you need to evaluate before buying a private real estate note?

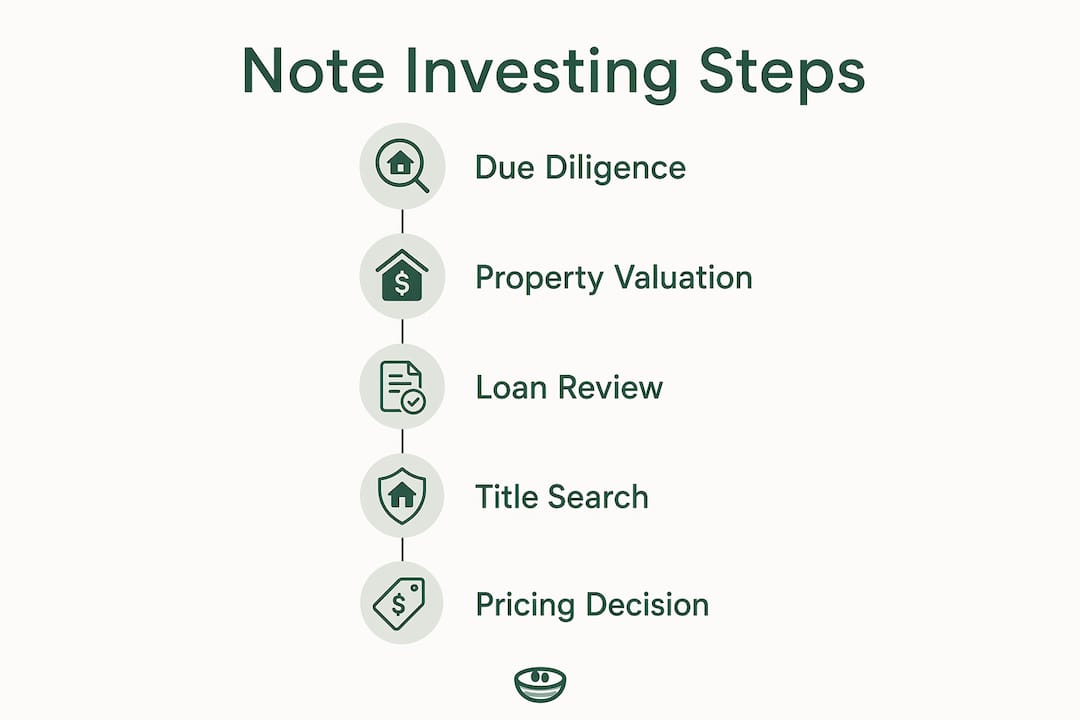

Due diligence is the single most important step in real estate note investing. Skipping it is how investors lose money on paper assets that look clean but carry hidden problems.

Property valuation

Start with the collateral. A Broker Price Opinion (BPO) gives you a fast, affordable estimate of the property's current market value. A formal appraisal costs more but carries more legal weight. Either way, you need to know the current value before you can calculate your loan-to-value ratio and decide whether the collateral adequately secures the debt.

Borrower and loan status

Review the borrower's payment history, credit profile, and current occupancy status. A borrower who is current on payments and living in the property presents far less risk than an absentee owner who is three months behind. Occupancy matters because vacant properties deteriorate faster and are harder to sell in a foreclosure scenario.

Complete loan documentation

Due diligence must include the original promissory note, the deed of trust or mortgage, a complete assignment chain, and any allonges attached to the note. Missing links in the assignment chain can make it legally impossible to enforce the note or foreclose. Never buy a note without a full collateral file in hand.

Pro Tip: Order a title search before closing on any note purchase. Title searches reveal undisclosed liens, tax delinquencies, and encumbrances that could wipe out your position entirely.

| Evaluation tool | Purpose | Typical cost |

|---|---|---|

| Broker Price Opinion (BPO) | Estimates current property value | $75–$200 |

| Formal appraisal | Legally defensible property valuation | $300–$600 |

| Title search | Verifies lien position and encumbrances | $150–$400 |

| Borrower credit pull | Assesses repayment likelihood | $30–$75 |

| Collateral file review | Confirms loan document completeness | Attorney fee varies |

How to calculate the right price to pay for a private real estate note

Pricing a mortgage note correctly is the difference between a profitable investment and a costly mistake. The goal is to pay a price that delivers your target yield given the note's interest rate, remaining term, and risk profile.

Here is a straightforward process for calculating your offer price:

- Identify your target yield. Decide what annual return you need. Most performing note investors target 8%–12%.

- Pull the note's payment schedule. Collect the interest rate, monthly payment amount, remaining balance, and months left on the loan.

- Discount the cash flows. Use a financial calculator or spreadsheet to find the present value of all future payments at your target yield. That present value is your maximum offer price.

- Adjust for lien position. First-lien non-performing notes trade at 30%–70% of fair market value, while second-lien non-performing notes trade at just 5%–25% of unpaid balance. Apply a steeper discount for junior liens.

- Factor in workout costs. If the note is non-performing, add estimated foreclosure costs, legal fees, and holding period expenses to your break-even calculation.

- Build in a foreclosure timeline buffer. Foreclosure timelines vary by state and can run 12–36 months. A note in a judicial foreclosure state like New York or Florida requires a larger price discount than one in a non-judicial state like Texas or California.

Pro Tip: Never price a non-performing note assuming a quick resolution. Budget for the longest realistic foreclosure timeline in that state, then stress-test your return at that worst-case scenario.

Entry-level investors can start with partial notes or distressed positions for as little as $5,000. First-lien performing notes typically require $20,000–$100,000 or more. That range means real estate note investing is accessible at multiple budget levels, but the risk profile shifts significantly as you move down the lien stack.

How does note servicing work, and why does it matter?

Performing notes require professional licensed loan servicers to handle payments properly. This is not optional. Federal and state regulations govern how mortgage payments are collected, how escrow accounts are managed, and how borrowers must be communicated with. Violating those rules exposes note holders to lawsuits and regulatory penalties.

A licensed servicer handles payment collection, escrow management for taxes and insurance, borrower correspondence, default notices, and year-end tax statements. Self-servicing often leads to regulatory and financial risks that far outweigh the cost savings. Servicer fees typically run 0.25%–1% of the outstanding balance annually, which is a small price for legal protection and accurate records.

Here is what to look for in a servicing agreement, and what to watch out for:

- Green flags: Clear fee schedule, licensed in the note's state, experience with both performing and non-performing loans, online borrower portal, and detailed monthly statements.

- Red flags: Vague fee structures, no state licensing documentation, no experience with default management, and slow response times to borrower inquiries.

- Best practices: Confirm the servicer carries errors and omissions insurance. Require monthly reporting. Set up automatic notifications for missed payments so you can act quickly.

- Warning signs for existing notes: Gaps in payment records, missing escrow statements, and borrower complaints about misapplied payments all signal servicing problems that need immediate attention.

Pro Tip: When you acquire a note, send a "hello letter" to the borrower through your servicer immediately. This establishes the new payment relationship, reduces confusion, and cuts down on missed payments in the first 90 days.

What are the common challenges in real estate note investing?

Note investing carries risks that differ from traditional property ownership, and most of them are invisible until you dig into the paperwork.

Title defects are the most common problem. A note secured by a property with a clouded title can be unenforceable. Experienced note buyers prioritize first-position lien verification at the title level and avoid second-position notes to reduce exposure. That discipline alone eliminates a large category of risk.

Borrower default requires a clear response plan. The three main workout options are loan modification, short sale, and foreclosure. Loan modification keeps the borrower in place and adjusts terms to restore performance. A short sale resolves the debt when the property value has fallen below the loan balance. Foreclosure is the last resort and the most expensive path.

Pro Tip: Verify lien position at the title level, not just from the seller's documents. Sellers sometimes misrepresent their position, and a title search is the only way to confirm what you actually own.

| Approach | Performing notes | Non-performing notes |

|---|---|---|

| Primary goal | Preserve cash flow | Restore performance or exit |

| Servicer role | Routine payment collection | Active default management |

| Typical workout | None needed | Modification, short sale, or foreclosure |

| Liquidity | Moderate | Low until resolved |

| Risk level | Lower | Higher, requires experience |

Note investing rewards patience and discipline, with diversification as the most reliable risk management tool. Spreading capital across multiple notes in different states and lien positions reduces the impact of any single default. Self-directed IRAs and Solo 401(k)s also allow investors to hold mortgage notes in tax-advantaged accounts under proper custody, which adds another layer of financial planning flexibility.

Key Takeaways

Private real estate note investing delivers consistent returns when investors combine thorough due diligence, accurate pricing, and professional servicing from the start.

| Point | Details |

|---|---|

| Yield range by note type | Performing notes yield 7%–14%; non-performing notes target 15%–50%+ with higher risk. |

| Due diligence is non-negotiable | Verify loan documents, assignment chain, title, and borrower status before every purchase. |

| Price to your target yield | Discount cash flows to your required return and adjust for lien position and foreclosure timelines. |

| Use a licensed servicer | Professional servicing protects you from regulatory violations and payment tracking errors. |

| Lien position drives risk | First-lien notes offer the strongest collateral protection; avoid second-lien positions until you have experience. |

Why I think most beginners price non-performing notes wrong

The appeal of being the bank is real. You collect interest income, skip the landlord headaches, and let a servicer handle the borrower relationship. I get why people jump in fast.

But the biggest mistake I see is investors underestimating operational complexity, especially on non-performing notes. They see a 40% discount on a note and assume the hard part is over. It is not. The hard part is the 18-month foreclosure in a judicial state, the property that needs $30,000 in repairs after you take title, and the servicer who does not specialize in default management.

Starting with performing notes is the right move for anyone new to this space. You learn how cash flow mechanics work, you build relationships with servicers, and you understand what a clean collateral file looks like before you ever touch a distressed asset.

Deal flow is also a relationship game. The most lucrative deals come from targeting owner-finance sellers directly through public records or direct mail. Those sellers rarely list notes in traditional marketplaces, so competition is low. Building credibility with note brokers by following through on commitments gets you access to off-market inventory that most investors never see.

My honest advice: treat your first three note purchases as tuition. Budget conservatively, hire a licensed servicer from day one, and do not skip the title search to save $200.

— Antony

How Nestnoted supports your note investment research

Evaluating a private real estate note means evaluating the property behind it. That collateral property is what secures your investment, and understanding its condition, location, and market value is not optional.

Nestnoted gives home buyers and real estate investors a private, organized platform to track and document properties they are researching. When you are assessing collateral for a note purchase, you can log property details, record your impressions after a site visit, and compare multiple addresses without losing notes in a spreadsheet or email thread. All entries stay confidential by default, so your research stays yours. Nestnoted is built for the kind of careful, detail-oriented work that note investing demands.

FAQ

What are private real estate notes?

Private real estate notes are debt instruments in which a borrower promises to repay a loan secured by real property. The note holder earns income by collecting interest payments without owning the physical property.

What yields can I expect from real estate note investing?

Performing mortgage notes typically yield 7%–14% annually. Non-performing notes target returns of 15%–50% or more, reflecting the additional risk and workout effort required.

How do I find private real estate notes to buy?

The most competitive deals come from targeting owner-finance sellers directly through public records searches or direct mail campaigns. Note brokers and online note marketplaces are additional sources, though competition is higher there.

Do I need a license to invest in private mortgage notes?

Investors who buy notes for their own portfolio generally do not need a license. However, servicing those notes, meaning collecting payments and managing borrower communications, requires a licensed loan servicer in most states.

What is the biggest risk in buying real estate notes?

Title defects and incorrect lien position are the most common sources of loss. A title search before every purchase is the most reliable way to confirm your position and identify undisclosed encumbrances.